The beleaguered US housing market is showing new signs of strain, with a surge in delistings, declining home sales, and growing unsold inventories raising concerns about a potential price correction. As reported in The Wall Street Journal, nearly 73,000 homes were pulled from the market in December 2024, a whopping 64 percent increase from the same month a year earlier. Despite an increase in available properties, the total number of home sales fell to its lowest level in nearly thirty years, suggesting that demand has suddenly dried up. Sellers of homes, which are usually the largest investment of an individual’s life, are reluctant to lower their prices and are instead delisting properties in hopes of better conditions in the spring. There are of course highly seasonal factors in housing market trends, and economic uncertainty under the new administration has vaulted in the past month, but there are deep structural issues — including mortgage rate lock-ins, regulatory constraints, and inflation-driven affordability challenges — distorting both the supply and demand sides of the housing market.

The persistence of mortgage rate lock-ins is one major factor. Homeowners who secured historically low mortgage rates during the pandemic are hesitant to sell, as moving would mean taking on significantly higher borrowing costs. That alone has reduced the inventory of homes on the market and artificially inflated home prices despite weakening demand. That effect can only last until homeowners find themselves forced to move due to job changes, family needs, or other life events that can no longer be postponed.

The number of homes for sale in December 2024 rose by 16 percent compared to the same period in 2023, indicating that some homeowners are finally re-entering the market. Even so, many sellers are choosing to delist their homes rather than accept lower offers. The result has been a “shadow inventory” of homes: those once on the market, now off, waiting to be relisted. Should sellers with homes suddenly be forced into the market by some macroeconomic shock — a recession, or something of that nature — the sudden glut of homes hitting the market could put substantial downward pressure on prices.

PMMS 30-year Fixed (black)

30-year Mortgage National Average (blue)

MB30 Index (orange), 2018 – present

(Source: Bloomberg Finance, LP)

At present, new home prices are starting to decline, but not necessarily due to an easing of market constraints. Builders, always conscious of the trends in markets, are increasingly building smaller, more affordable homes for the first-time buyer market. While that helps some would-be homeowners, it underscores the broader affordability crisis. Some homebuilders are also offering incentives, such as mortgage rate buy-downs (a financing arrangement where a homebuyer pays an upfront fee to a lender to permanently reduce the interest rate on a mortgage), but even those measures are proving insufficient in some cases.

The number of completed but unsold new homes rose by nearly 50 percent in December compared to the previous year, reflecting the gaping mismatch between what prospective homebuyers can afford and what the supply side of the market is offering. A smoother adjustment might be found if there were a relaxation or elimination of the restrictive web of zoning laws and permitting regulations, which severely constrain the supply of housing in high-demand areas. Without reforms to these policies, the market will continue to struggle to meet real housing needs, and affordability challenges will persist, perhaps worsening.

Inflation and rising mortgage rates are additional obstacles to a housing market recovery. The average 30-year fixed mortgage rate approached 7 percent at the end of 2024, making homeownership more expensive and suppressing demand. Higher borrowing costs, alongside elevated home prices, have kept many potential buyers on the sidelines. Uncertainty about the direction of the economy under the new administration, as seen in the sudden decline in both business optimism and consumer sentiment, also play a role. Real estate investment firms like Invitation Homes and American Homes 4 Rent are trading at deep discounts to their asset values, indicating that investors are expecting a housing market correction. The jump in delistings suggests that sellers would prefer not to cut their listing prices, but if demand does not return they are likely to be forced to do so. The longer that unsold home inventory remains high, the more likely a broader housing market correction becomes.

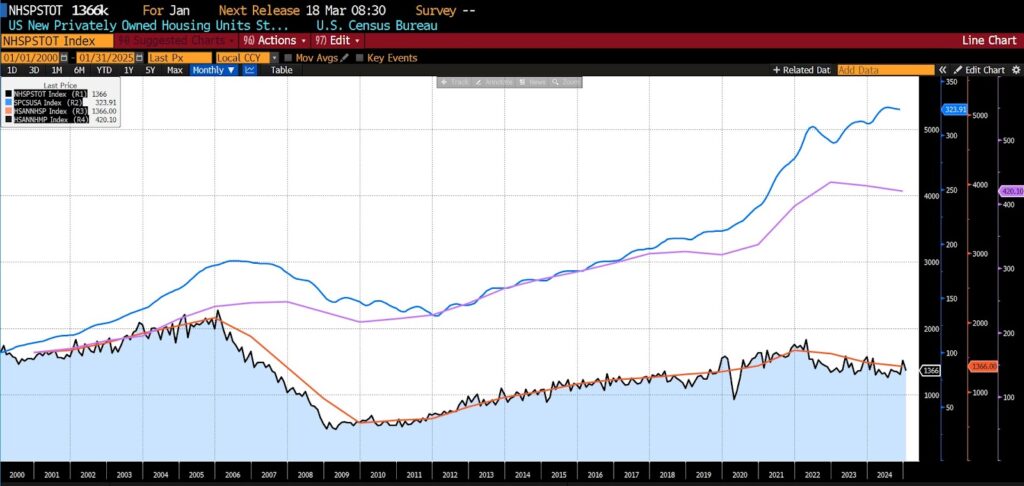

New Home Sales, Median Price (violet)

S&P CoreLogic Case-Shiller US National Home Price Index (blue)

Annual US Housing Starts (orange)

US New Privately Owned Housing Units Started by Structure (black)

(The violet and blue lines represent two measures of median home price trends over the past 20 years, while the black and orange lines track housing starts. The sharp increase in median home prices, coupled with a decline in new home construction, is evident.)

A useful economic concept to understand these dynamics is the reservation price: the lowest price at which a seller is willing to engage in a voluntary transaction. It is typically a price that exists in the mind of a seller or buyer, as economic actors try to maintain negotiating leverage and maximize their utility. Typically in a market downturn the most motivated sellers lower their reservation price to meet buyers where they are. In the current housing market, though, many sellers are reluctant to adjust their expectations downward, even in the face of weak demand. This is why delistings have surged rather than outright price declines: sellers’ reservation prices remain above what buyers are willing to pay. To some extent, that may suggest optimism about the economy broadly, or the housing market specifically. If housing market conditions fail to improve, sellers will have to reduce their reservation price or risk being unable to sell their properties. The longer the standoff persists, the greater the likelihood of a sharper price correction when sellers finally capitulate.

The mortgage rate lock-in effect stems directly from the Federal Reserve’s decision to pursue zero interest rate policies (ZIRP) during the pandemic, which has generated an unnatural incentive for millions of homeowners to stay put. Regulations at many levels — including zoning laws, permit restrictions, environmental review processes, and other hindrances — are continuing to stifle housing supply, preventing the market from adjusting, let alone clearing. And inflation, which has by some measures been rising since the Fed began lowering rates in September 2024, has eroded purchasing power and made homeownership all the less achievable. New home construction, as well, is being constrained by burdens that increase costs and slow the pace and breadth of development.

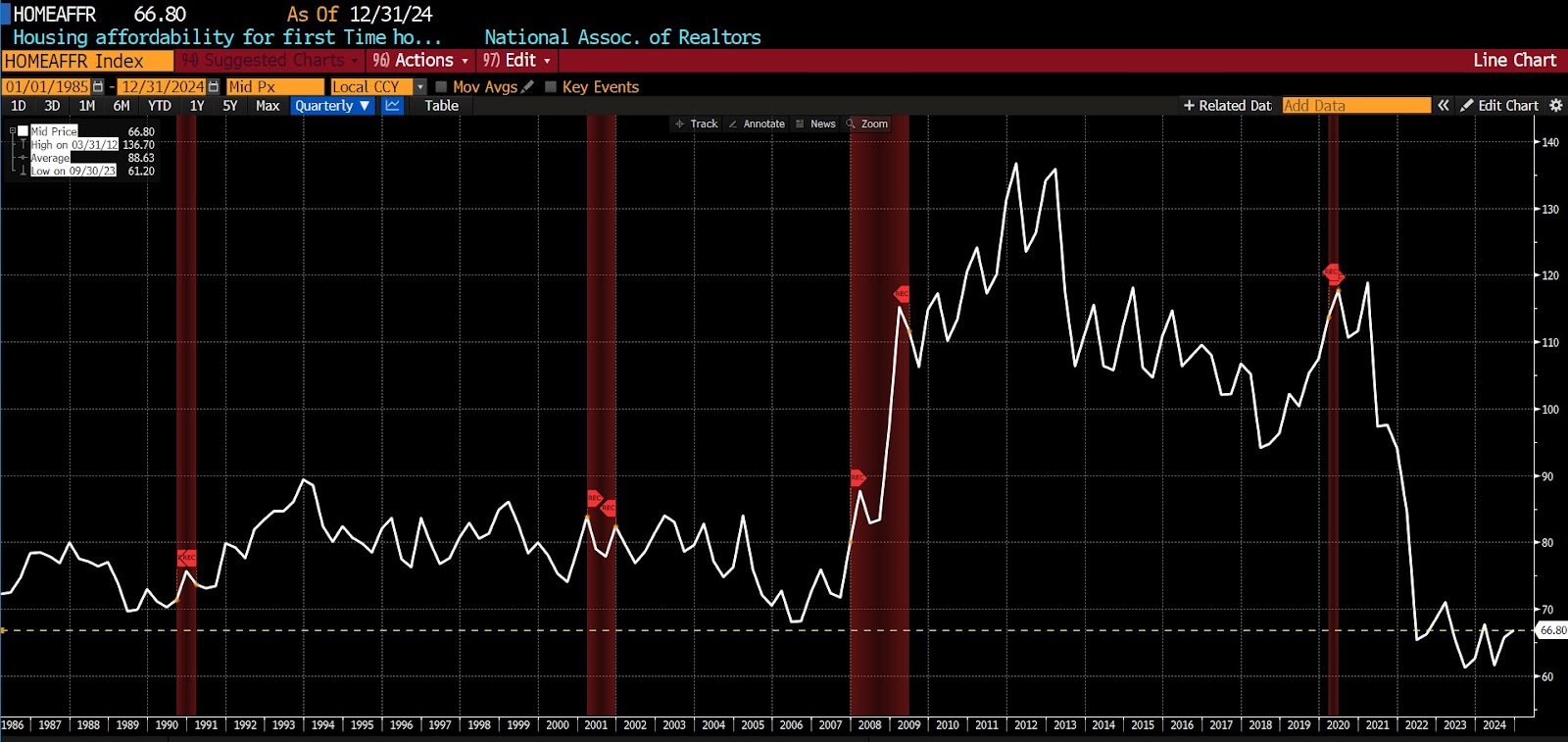

Housing Affordability for First Time Homebuyers, National Ass’n of Realtors, 1986 – present

(Although off the lows of late 2023 and mid-2024, home affordability is still, in early 2025, lower than it was in the depths of 2006.)

Allowing interest rates to find a natural equilibrium, whether that is higher or lower than the Fed-divined level, would help restore balance between both the supply and demand on the loan market and, subsequent to that, in housing. Rolling back restrictive zoning laws and easing or eliminating the permitting process would allow builders to create more housing where it is needed most, sending market signals to suppliers. And reducing purchasing-power-destroying, budget-winnowing inflation would ease the crisis of affordability. In other words, let markets work instead of waiting for a “soft landing” or plotting another round of grossly wasteful government stimulus.

The current wave of delistings, declining home sales, and rising unsold inventory are a warning sign that the US housing market is ailing and possibly bound for a sharp, perhaps sudden drop in prices.

The effects of the mortgage rate lock-in are fading, albeit slowly, yet affordability remains a major concern due to high interest rates, regulatory constraints, and inflation. Sellers with high reservation prices may not be able to hold out much longer, and if they all adjust their prices downward at roughly the same time, it will send a discounting cascade through the market. Ensuring a healthy, stable housing market requires allowing supply and demand to realign via market forces rather than imposing still another layer of costly, distortive rules to a market already piled high with them.